Last editedApr 202311 min read

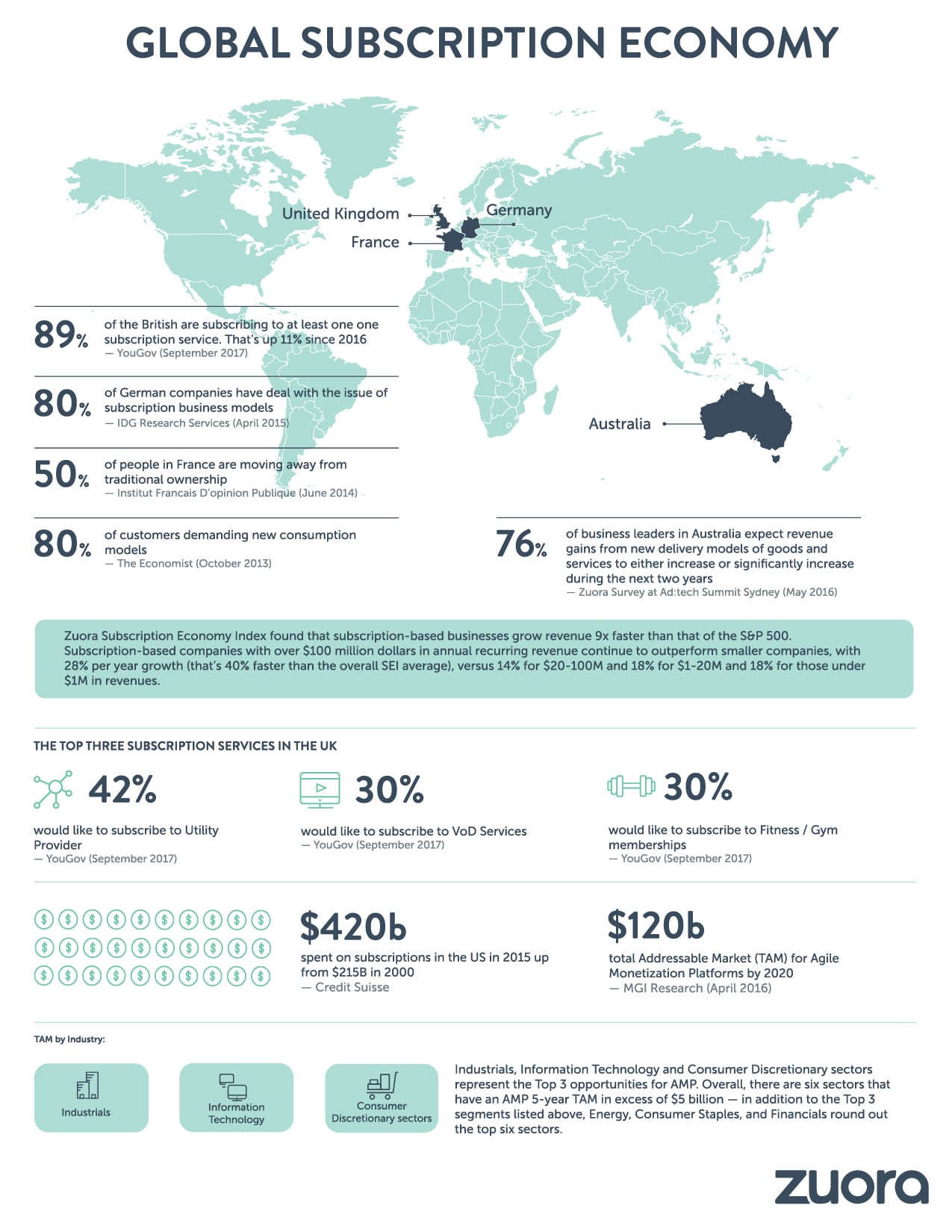

Subscription services have taken off in the UK in the last few years. 89% of British people are now subscribing to at least one subscription service, while in the US, $420bn was spent on subscriptions in 2015, a 95% increase since 2000.

Businesses offering subscriptions, memberships and payment plans can choose a number of methods to manage regular payments, including recurring card payments (via continuous payment authority), Direct Debit and standing order.

This guide covers everything you need to know about taking regular payments from your customers by credit or debit card, as well as a comparison with other payment methods available to you.

What are Continuous Payment Authorities?

A recurring credit card payment, often referred to as a Continuous Payment Authority (CPA), is an authorisation provided by the customer that permits the merchant to take payments from them by either debit or credit card. These payments will remain in force until the customer cancels the arrangement.

A CPA enables the merchant to take payments from a customer’s account on dates of their choosing, and for different amounts, without seeking further authorisation from them.

Continuous Payment Authorities can be set up online, in person or over the phone. To give a merchant a Continuous Payment Authority on a card account, the customer provides their debit or credit card details (rather than their bank details, which would normally be used to set up a Direct Debit).

GoCardless makes it easy to collect Direct Debit payments on your Xero invoices. Automate Direct Debit payment collection. Reduce manual admin. Get paid on time, every time

Example uses of CPA payments

Continuous Payment Authorities are used by the likes of gyms, internet service providers and payday loan companies.

A Continuous Payment Authority could be:

For a regular payment, usually of a fixed amount

For a less frequent but also regular payment

For a one-off amount to be paid in the future

The Consumer Contracts (Information, Cancellation and Additional Charges Regulations 2013 set out how merchants should act in setting up a Continuous Payment Authority and during its lifetime.

How to collect payments with GoCardless

1.

Create your free GoCardless account, access your user-friendly payments dashboard & connect your accounting software (if you use one).

2.

Easily create payment links to collect one-off or recurring online payments, and share them with your customers.

3.

From now on you'll get paid on time, every time, as GoCardless automatically collects payment on the scheduled Direct Debit collection date. Simple.

Continuous Payment Authorities for merchants

When to use a Continuous Payment Authority

Continuous Payment Authorities are a common way to take recurring payments from customers.

They provide businesses with regular sales opportunities and predictable cash flow. Payments are charged automatically and customers receive their orders without any extra activities.

Continuous Payment Authorities are particularly good for:

Transactions which need immediate clearing or next-day payment. E-commerce services such as Amazon Prime often use Continuous Payment Authorities for recurring subscription fees, as does Transport for London for automatic Oyster top-ups.

Liquid assets and high value goods, such as cars or currency, where other recurring payment methods like Direct Debit are not suitable (because around them could make these a target for fraudsters).

Continuous Payment Authorities are not so good if:

You’re a membership or subscription business and want to reduce payment failures. Recurring card payments typically have higher payment failure rates than other recurring payment options like Direct Debit, as card details expire and cards are often lost or stolen.

You want to reduce costs per transaction: recurring card payments tend to cost more than other payment methods like Direct Debit and standing order.

How to get access to a Continuous Payment Authority

In order to get access to a Continuous Authority Payment, you must first take a standard payment from the customer. This will include the capture of the card security code (CV2) and the expiry date.

Upon successful completion of the payment, the merchant is able to perform a repeat against the transaction.

The amount of the original payment does not matter when performing a repeat. The merchant is able to repeat the transaction for any amount below or above the previous payment or repeat.

Making Changes to a Continuous Payment Authority

The UK Cards Association observes that the merchant should only make changes to the Continuous Payment Authority, such as the amount or timing of payments, with the customer’s clear consent. “It is good practice for the merchant to provide the customer with either a brief statement each time a payment is taken or a summary annual statement,” it says.

The UK Cards Association adds that, if a Continuous Payment Authority is being renewed for an additional fixed period, this should be treated as setting up a new Continuous Payment Authority and the process above should apply: “If your card expires during the course of your Continuous Payment Authority, you should check with the retailer whether your new card details have been automatically updated with them, as this will not always be the case.”

“If you switch bank account your Continuous Payment Authority will not be transferred across to your new card, so you will need to contact the retailer with your updated details.”

Which is best for your business: Continuous Payment Authorities, Direct Debit or standing orders?

Continuous Payment Authorities, Direct Debit and standing orders are all automatic payment methods used for collecting regular payments.

Continuous Payment Authorities use credit and debit card networks, whereas Direct Debit and standing orders are a form of bank to bank payment.

Here we lay out the upsides and downsides of Continuous Payment Authorities (CPAs) for merchants, when compared to Direct Debit and standing orders.

| CPAs | Direct Debit | Standing orders | |

| Set up | You're in control. You control set up, amount and date of payments. You may have to go through added hassle of getting a merchant account. | You're in control. You control set up, amount and date of payments. With GoCardless you can choose to set up your own merchant account or use GoCardless as your merchant account. | Customer is in control. Customer controls set up and you're dependent on them. Unfeasible if you have > 25 customers. |

| Speed of payment | Fast. Varies by provider, but providers like PayPal offer 24-hour turnaround - even for initial payments. Best used if you require next-day payment. | Medium. Initial payments through Direct Debit can take six working days while the funds clear. Subsequent payments clear completely on the fifth working day. Find out more about Direct Debit timings | Fast. With Faster Payments, standing orders are usually processed and received on the same day they're sent. |

| Flexibility | High. You can charge fixed or varying amounts, and you don’t have to specify a date when you're going to take a payment. | Medium-high. Charge fixed or varying amounts and change amount or date of payment without customer's authorisation. You need to give advance notice of payments (default is 10 days). GoCardless reduces advance notice to 3 days and takes care of the messages. | Low. You can only take fixed amounts at regular intervals. Any changes have to be authorised by the customer. |

| Cost | High. Around 3% + 20p per payment and monthly fee for merchant account. Likely to be admin costs involved in chasing customers to update expired card details (at least every three years per customer) or additional costs for account updater services. | Low. Varies by provider but expect to pay 20 - 40p or 1% per transaction, with no hidden costs. Free to use GoCardless as your merchant account, or pay a monthly fee for your own merchant account. | Low. Possibility of a small fee taken by your bank, but otherwise free. Likely to be admin overheads associated with managing standing orders. |

| Reliability and customer retention | Medium. Payment failure rates vary, but tend to be greater than 5%, due to cancelled and expired cards or customers hitting spending limits. Account updater services help mitigate this. See Reliability and customer retention section below. You may be charged for failed payments. | High. Since Direct Debit avoids card networks, payment failure rates are typically low, at less than 1%. Providers like GoCardless only charge you for successful transactions. | Medium. Avoids card networks, so payment failure rates of less than 1%. But you won’t be notified if a payment fails (e.g. if there are insufficient funds), so you'll have to check accounts manually and chase up customers. |

| Customer protection | Medium. Continuous Payment Authorities enable customers to apply for a refund when using credit cards, but there are greater limitations for customers than when using Direct Debit. | High. The UK Direct Debit Guarantee offers a high level of protection for customers, allowing them to apply for an immediate refund from your bank if they believe a payment has been mistakenly taken, with no time limit attached. For most businesses however, the risk of chargebacks is low. See Customer Protections section below. | Low. No customer protection once payments are made which gives merchants greater protection. |

Reliability and customer retention

Recurring card payments are more likely to fail than Direct Debit payments, leading to revenue loss, as well as unhappy customers. Reasons include cancelled cards (cards are often lost or stolen), expired card details or customers hitting spending limits.

Payment failure rates vary, but for Continuous Payment Authorities they tend to be greater than 5%.

There are solutions available to help increase reliability of card payments and reduce associated customer churn. These typically fall into two categories:

Reactive solutions which aim to stop card failures turning into customer churn, by automatically retrying card payments at specific intervals or by trying another Card on File (CoF) assigned to the customer.

Proactive solutions like account updater services run by card networks like Visa and Mastercard, which aim to prevent card failures happening in the first place by batch-checking card details with the issuing banks. Merchants can access these directly from card network providers like Visa or via an acquirer like Adyen, Braintree and WorldPay (acquirers may build their own logic on top of the basic account updater service, for example allowing you to run a report as to which details were updated and what was changed). In addition, billing platforms like Zuora offer this service as an add-on to customers.

Card updating services are available in US, Canada, UK and parts of Europe, where these services are fairly mature and widely used by subscriptions businesses.

The service is not currently available everywhere however, since it requires local issuing banks' processors to opt into and integrate with the scheme, which takes time and effort to implement.

It’s worth noting that even in markets where these services are mature, cards may slip through the cracks for a variety of reasons. In the US for example, while it is now mandatory for issuing bank to participate in these schemes, there are still banks whose haven’t yet integrated.

Cards from banks that are not in the scheme will not be picked up by account updater services. Other cards that may fall through the cracks include international cards, prepaid cards and cards belonging to unsupported card networks.

Cards may also be missed by account updater services if a bank fails to promptly update Visa and Mastercard about a change in card deatils (since many smaller banks still rely on manual processes), or if a customer switches card provider.

When it comes to costs, Visa and Mastercard charge for these services. Payment processors like Braintree, Adyen and WorldPay, and billing platforms like Zuora may pass these costs on directly to merchants for example by offering the service as an add-on, or they may bake them into overall service costs.

It’s also worth noting that these technologies require customer card details to be stored in multiple locations, which brings with it associated security risks.

Since Direct Debit and standing orders avoids card networks, payment failure rates are typically low, at around 1 or 2%.

If you choose to use automated Direct Debit, with a provider like GoCardless, you can significantly mitigate the risk of late payments.

Since GoCardless optimises the Direct Debit process, our customers enjoy low transaction failure rates. In case, we only charge you for successful transactions.

Customer protections

Continuous Payment Authorities enable customers to apply for a refund when using credit cards, but there are greater limitations for customers than when using Direct Debit.

With Direct Debit, the UK Direct Debit Guarantee offers a high level of protection for customers, allowing them to apply for an immediate refund from your bank if they believe a payment has been mistakenly taken, with no time limit attached. This ‘chargeback’ or indemnity claim process, has led to some fraudulent activity, with customers asking for refunds they are not entitled to.

The risk of this is higher for businesses in some industries, including gambling, car sales and other high value physical goods. For these reasons, it’s not recommended for businesses in these industries to use Direct Debit.

For most business however, the risk of chargebacks is low. However, having the Guarantee in place, does make Direct Debit one of the UK’s most trusted payment methods. For more information on this, see: Don’t fear the Direct Debit Guarantee

Getting paid shouldn't cost you time, money and stress!

That's why GoCardless automates payment collection to make it simple, affordable & hassle-free.

Continuous Payment Authorities for customers

How to tell if you have a Continuous Payment Authority on your card

This is not always a straightforward process as it can be unclear when you sign up to a service that you're setting up a Continuous Payment Authority. If you have regular payments appearing on your credit card statement that you don't make in person or online, this is probably a Continuous Payment Authority in action. Again with payments debited from your current account; if these are not listed as direct debits or standing orders, they are probably Continuous Payment Authorities.

Setting up a Continuous Payment Authority

You can set up a Continuous Payment Authority with a business or organisation if you agree to them taking regular payments from your bank account.

How to cancel a Continuous Payment Authority

Prior to 2013, it was very difficult to cancel these payments. The [Financial Conduct Authority FCA found that card issuers, such as banks and building societies, were not always cancelling Continuous Payment Authorities when their customers asked them to.

By way of example, in 2012 the BBC reported that Lloyds TSB and Santander admitted denying some customers their right to cancel recurring payments. The UK regulator subsequently tightened up its procedures to make sure, when consumers cancel, the money stays in their account.

In most cases, customers should be able to cancel by contacting the company taking the payment and asking it to stop. However, they do have the right to cancel directly with their card issuer. Once they have done this, it must stop payments immediately – it cannot insist that a customer first agrees this with the company taking the payment.

However, customers should inform both the company taking the payment and their card issuer when cancelling a Continuous Payment Authority. They may also want to check their next statement to ensure the payment has been cancelled as requested.

Customers should keep in mind they will still be responsible for paying any money that they owe.

Getting a refund for Continuous Payment Authority you didn't realise had been set up

For Direct Debit, there is the Direct Debit Guarantee but there is no such equivalent in place to protect consumers against administrative errors when processing Continuous Payment Authorities. This means that the company who made the charge decides how they will deal with any request for a refund.

Do Continuous Payment Authorities end if I close a card account?

Some card issuers may still honour transactions made on a card after you request your account to be closed and you will need to cover these. This should only be for a short period after closure, however.

Do Continuous Payment Authorities get transferred if I move my current account to another bank?

Remember that Continuous Payment Authorities are linked to cards rather than bank accounts. The Current Account Switch Service launched in September 2013 and is a free-to-use service for consumers, small charities, small businesses and small trusts that aims to make switching current accounts simple, reliable and stress-free.

It moves Direct Debit instructions and standing orders that are linked to your current account, but not recurring payments on a card. If you wish to keep paying a provider in that way, you'll need to inform them of your new card details as issued by your new bank.

Payday loans

The Financial Conduct Authority (FCA) notes that: “When taking out a payday loan, it is common for the lender to set up a Continuous Payment Authority on a debit card. However, we sometimes hear of payday lenders varying the dates and amounts they claim from customers’ accounts and making repeated attempts to take payments.”

FCA research found that some card issuers were calling Continuous Payment Authorities set up with a payday lender’s ‘guaranteed payments’ and incorrectly refusing to cancel them when requested by their customers. Those card issuers have now agreed to end this practice.

As the FCA points out, consumers should note that, no matter if the firm they are dealing with calls itself a Continuous Payment Authority a ‘guaranteed payment’, ‘recurring payment’ or ‘recurring transaction’, it is still their right to cancel it directly through their card issuer.

If I cancel a recurring transaction, will it stop?

To quote Nationwide Building Society: “Your request may not immediately stop further payments being taken from your account. Where a company continues to take payments from your account after we know you have withdrawn your consent, we'll refund that money to you.”

Nationwide Building Society recommends that you also contact the company directly to make them aware that you've cancelled the payment, because this payment arrangement may be part of a contract between you and them for the service you requested, and you'll want to be sure that they know that this is no longer required. This policy applies to all our debit, cash card and credit card customers.

What to do if payments are not cancelled

Any related payments taken after a customer has asked for a Continuous Payment Authority to be stopped are considered to be unauthorised transactions. Card issuers must refund these payments and any related charges immediately.

If payments continue, contact the card issuer to arrange a refund. If it fails to do so, customers should make a complaint to the card issuer and, then, if they are not satisfied with its response, take the complaint to then Financial Ombudsman Service

Can a recurring card payment/Continuous Payment Authority bounce?

Yes, although if payment is due on the 1st of each month, for instance, and on that day there isn't enough money in the customer’s account, the next step would be to attempt the 2nd, 3rd, 4th, 5th etc until there are sufficient funds.

What’s the difference between Continuous Payment Authorities, Direct Debit and standing orders?

Continuous Payment Authorities, Direct Debit and standing order are two popular ways you can make regular payments to a company for goods or services.

With a Continuous Payment Authority, the customer gives an organisation their card details. The organisation will ask for a credit or debit card number, rather than bank details.

With Direct Debit, the customer authorises an organisation to take money from their bank account for a fixed or variable amount.

With standing orders instructs their bank to make fixed payments at regular intervals to a company.

Here we lay out some of the things to bear in mind when deciding between these payment options.

Type of purchase

Recurring card payments Customers increasingly view credit and debit cards as a safe and convenient way of paying for one-off goods and services in shops or online, anywhere in the world.

Direct Debit Direct Debit payment is regarded as more appropriate for regular payments, for example, mortgage payments and electricity/gas accounts as well as other types of regular payment, including subscriptions, memberships and paying for goods or services by instalment.

Standing orders Standing orders only allow you to pay fixed amounts at regular intervals - so if the payment amount or date might change, for example if it is based on usage as in the case of energy bills, Direct Debit is more suitable.

‘Perks’ of usage

Some customers prefer using credit cards over standing orders and Direct Debit, since they can earn loyalty points, air miles and other benefits, based on usage.

It’s worth bearing in mind however that these perks might come at a cost: if merchants are being charged fees for credit cards transactions, they may pass these costs on to you as a customer in the form of additional fees or surcharges on your transaction.

Cancellations

Recurring card payments Cancelling a recurring card payment is not as straightforward as cancelling a Direct Debit or standing order.

When cancelling a credit card, the account stays open for a few more months to ensure all payments made on the card are processed. If the recurring payment is still being requested by the organisation, it will count as a new incoming payment, causing the account to remain open and the organisation asking the customer to settle payment.

Direct Debit Under the Direct Debit Guarantee, customers have the right to cancel a Direct Debit at any time by contacting their bank. Depending on the contract, the customer is also advised to also confirm the cancellation with the organisation.

Standing order Since a standing order is set up by you, you can change or cancel it via your bank without notifying the company you are paying.

If you decide to cancel a standing order, you can do so at any time. You'll need to speak directly to your bank or building society, but you should let the person or company that usually receives the payment know in advance, so you don't risk any fees or charges for non/late payment. As a standing order can only be created or instructed by yourself, once the money leaves your account it cannot be recalled.

Customer protections

Recurring card payments Continuous Payment Authorities don’t offer as much protection for customers as Direct Debit. When using a recurring card payments, there have been instances of merchants taking more from a customer’s bank account, or changing the date they do it, without giving them notice.

With Continuous Payment Authorities, bear in mind that you're effectively giving a company the right to debit your account without notice. Ultimately, a recurring card payment enables a company to collect payment whenever they want and for whatever amount they think the customer owes them.

Reputable companies will do the right thing when operating as a Continuous Payment Authority, but critics point out that not everyone in the marketplace behaves impeccably.

There have been issues with companies who don't make it clear that you're agreeing to a Continuous Payment Authority. Free trials online sometimes require you to enter card details and if you don't cancel during the trial period, you can find your card billed as part of a rolling subscription on a Continuous Payment Authority.

Direct Debit With Direct Debit, the Direct Debit Guarantee is in place to protect customers. Organisations using the Direct Debit Scheme go through a careful vetting process before they're authorised, and are closely monitored by the banking industry. The efficiency and security of Direct Debit is monitored and protected by a customer’s bank or building society. The Direct Debit Guarantee applies to all direct debit payments. It protects customers in the rare event that there is an error in the payment of a Direct Debit.

Standing order In the case of standing orders, no legal or regulatory customer protection exists once payments are made, though your bank may be able to help reclaim funds for you.

{kind=link}